Look back in anger or disruption that incumbents can love - AgTech in the 2010s

The first Italian Republic, said to have lasted from 1946 to 1992, collapsed as former Prime Minister Bettino Craxi fled into exile to escape charges of corruption during his tenure in power. 1992 was supposed to be the rebirth of Italy, with the old order discredited and deposed, and Silvio Berlusconi[1] poised to lead the country to a better kind of politics. As events were to subsequently show, the First Republic, in all its ignominy, was to be replaced by an even more disappointing Second Republic that faced charges of corruption on far more monumental scale. Observers of Italian politics ruefully trotted out that very Italian term ‘Transformismo’ – the transformation of a political force by osmosis into what it was supposed to replace[2] - to explain how an entire order was converted into exactly what it was intended to change.

AgTech and the promise of disruption

So why does an overview of AgTech in the past decade start with an invocation of Italian politics, interesting as it maybe? As someone who has tracked this space for about half a decade, I sometimes sense a reflexive attitude in the sector towards any critique, with success equated to existence, i.e. AgTech will transform the world because the world needs to be transformed. My argument in this article is that a retrospective view over the past decade or so cannot but arrive at the conclusion that till now, AgTech has been more than just the God that failed, it is the Rebel that has been tamed. From a Venture Capital perspective, the body of evidence that points in that direction is quite undeniable. Whether it is the limited number of exits (and the iconic one was achieved back in 2013 before the influx of VC dollars into AgTech); the rising body count of companies going out of business; or the fact that no more than a handful of companies in AgTech have meaningful revenues; the sector is currently seeing a reassessment which contrasts markedly with the optimistic hopes expressed for the revolutionization of Agriculture till quite recently. Lux Research even acknowledged this trend, conceding that their exuberant hopes for the adoption of drones in agriculture, expressed in 2014, had not materialized as late as of 2018.

If this was just a case of technology not being adopted as fast as expected, AgTech would be no different from so many other technology segments. However, the problem with AgTech is something far more deep rooted. In conversations with startups, investors and corporates, one can detect a distinct change of tone. No longer are startups talking about displacing the incumbent industry – most are now talking about co-existence or even more dramatic levels of dependency on incumbents. While trade sale is a legitimate route to exit for a startup, there is no fear of missing out on anything that is driving corporates to look at acquiring startups. Corporate acquirers face a landscape that is fast becoming a buyer’s market, with numerous startups putting themselves up on the auction block at single digit million revenue levels, perhaps the single most striking trait of the current AgTech landscape.

Say it out softly – there is no disruption in AgTech. Ambitions have mellowed. Valuations will follow. AgTech in the 2010s was essentially off balance sheet R&D for Big Ag and now the prodigal son wants to return home. AgTech isn’t displacing the incumbent industry, it is replicating it. Transformismo.

Destiny disrupted

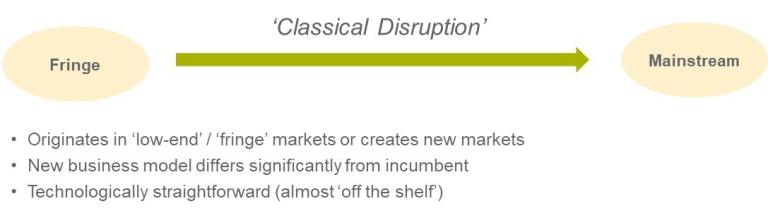

So why has AgTech not delivered on the promise of disruption? The reason, I argue, is that it never conformed to the definition of disruption in the first case. While disruption is a much misused and abused term; technology, innovation and the Venture Capitalists who finance them would wither away if one didn’t believe that disruption, like true love, is real[3] and even if it cannot be adequately articulated, you would know it once you experience it. So in the spirit of being a believer, I go back to the classical definition of Disruption with a capital-D, as pronounced ex-cathedra:

With the clarity of the creed, it isn’t difficult to see that AgTech as it exists violates nearly every single one of the late Professor’s criteria for disruption.

The challenges of AgTech might now be patently obvious – in the 2010s, AgTech investment was disproportionately oriented towards markets whose farmers are among the most efficient in the world and developed products that were expensive and didn’t offer a clear ROI. The guiding principle of AgTech may be legitimately summarized as a modified version of Say’s Law in economics

Say’s Law of AgTech = Technology creates its own Markets

With a decade of empirical evidence, this implicit principle of AgTech can be discarded. Technology for technology’s sake, being crammed down the throats of customers who ultimately operate in a declining commodity market, doesn’t create a viable business.

Involution

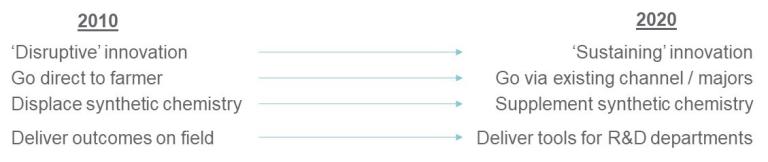

The saving grace for AgTech in the 2010s was that at least from a technology perspective, there was significant experimentation, especially within the digital segment, that was differentiated from the internal R&D programs of the majors. However, if the assessment paradigm changes to business models, the industry could be legitimately characterized as a tautomer of the existing system. AgTech has not delivered any new business models, or crashed timelines or costs of bringing technology to markets, nor brought any new segments of under-/non-consumption into the fold of the market. The 2010s began with radical ideas of trying to go direct to customers (most notably for software), cutting out the agronomists (for advisory services) and capturing value by going all the way downstream (mainly for biologicals). By the end of the 2010s, nearly each of the preceding goals has been abandoned, as startups struggle with generating commercial traction. Perhaps the best illustration of this trend is the biologicals segment, where the early belief that we might soon live in a world without synthetic chemicals, is now under serious reassessment, alongwith the hefty valuation bubble it helped engender.

The promise behind the biologicals revolution in Agriculture was predicated on the high returns that VC has seen in the pharma space. However, some key differences need to be highlighted. Firstly, pricing power in Agriculture is nowhere close to Pharma, because at the end of the day, corn is a commodity and human life is not. Secondly, the major returns in Pharma are coming from the use of technologies to treat / cure conditions for which there was no prior respite. In Agriculture, new and expensive technologies are being used to deliver essentially the same end results as the incumbent industry. The appropriate analogue in Pharma would be if millions of dollars of capital were going into companies looking for a new way to cure Malaria. Lastly, biologicals remain compounds that have an impact on environment and living organisms, hence the most expensive and time consuming part of the development process remains the trialing and regulatory phase, and few startups have offerings that substantially crash the time to market. Thus, the insurgents end up replicating the incumbents, subject to the same long commercialization cycles with heavy upfront investments – and limited value prospects at the end of it all. The irony here is that Biologicals is probably the one segment of AgTech where there is a real demand, driven by customer preferences and regulatory intent. However, at least in the near term, this is more likely to benefit established players in the biologicals space, who offer Big Ag companies a quick route to market, established markets and customers and ready revenues, rather than startups that still need to invest large amounts of money for long periods of time in the discovery phase, while ultimately leaving the risks associated with development to Big Ag.

Whither AgTech or Wither AgTech?

The polemical excursus above should also explain one of the frustrations that many of the investors in the sector have – where are the exits? The answer is that there is no compelling reason for any of the large companies in Ag (or even outside) to acquire startups. Companies looking for an inorganic boost to revenues cannot look to AgTech acquisitions as nearly 90% of startups have annual revenues under $10m. The same revenue sluggishness rules out the IPO route for most startups, with the rule of thumb being that a company should have stable revenues of $100m before tapping the capital markets. Few AgTech companies have gone down that route and the post-IPO share performance of the few that have would serve to only prove the point. The representative AgTech exit thus is probably the acqui-hire, whereby companies look to acquire startups for the teams and technical capabilities they bring, however these tend to be early stage, small ticket and in a consolidated industry, one has to assume there is limited appetite for too many more of these.

A brave new world

Ultimately, like the famous senator, I come not to bury AgTech, but to praise it. Firstly, for all the challenges in the ecosystem, they do not reflect on the hardwork and commitment applied in this space by so many founders and teams of passionate individuals, people who I am privileged to associate with on a regular basis. Neither do I think that startups and founders should be obsessed on being 'disruptive' as that is not the only way to create value; after all, the 'success' story that is Uber is not an example of disruptive innovation. AgTech does indeed hold the potential to create value for the evolving Agri-Food system (and it is definitely evolving – more on that in a future post!). However, to succeed in doing so would require a shift away from the ‘foie gras’ mindset of furiously injecting technology down the throats of recipients who clearly are in two minds about the benefits of the whole thing, if not outrightly skeptical. AgTech in the 2010s was hardly bold – it needs to be much bolder in the 2020s. Can it look towards un/under-served customer segments? Can it improve the cultivation of crops overlooked by the food system? Can it create markets where none previously existed? The wellwisher of the sector must hope so, otherwise the whole sector will go through yet another cycle of inflated expectations and crashing disappointments. After all, Silvio Berlusconi was appointed Prime Minister 4 times in total.

[1] No, really

[2] I am indebted for this summary piercing analysis of post-war Italian politics and for the concept of Transformismo to the immaculate Perry Anderson

[3] I couldn’t help but chuckle at these lines “Whether or not Disruption Theory can predict the future isn’t a matter of opinion, it’s a matter of fact”, which sound almost like a parody that I would have been proud to write

{kind=link}

{kind=link}