The European opportunity for digital agriculture

A spectre is haunting Europe – the spectre of digital solutions that fail to live up to the hype and disappoint the expectations of growers, start-ups and VC investors. While it might be harsh to single out Europe over this state of affairs, it is equally necessary to recognize that the unique, structural characteristics of Agriculture in Europe that make it imperative for digital solutions to be customized for the needs of European farming, rather than being epigones of digital offers tried and tested across the Atlantic.

European farming and the subsidy landscape

The strategic value of secure food supplies has made it a priority of governments right from the time of the bread and circus policies of Imperial Rome. In post-war Europe, governments sought to exorcise the memory of war time shortages through the Common Agricultural Policy that operated through price guarantees to support intensive farming in pursuit of increased production levels. The centrality of the CAP to the European integration project can be highlighted by the fact that the CAP accounted for ~75% of the EU’s budget expenditure in 1985 and even today, after a series of reforms, it still is the single largest item of the EU budget, coming in at ~30% of the budget at ~€40bn.

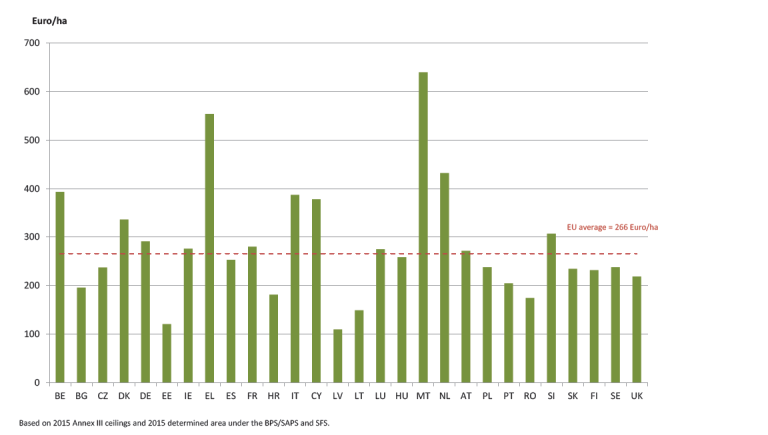

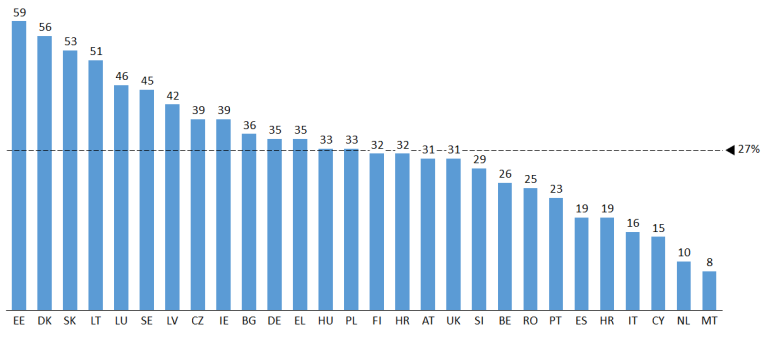

The bulk of this spend goes through a subsidy mechanism known as Direct Payments to growers, which is akin to a minimum income guarantee to growers without which most would struggle to remain profitable against global agricultural competition. The centrality of this subsidy can be seen from the fact that on average, an EU farmer receives €266/ha[1] from the Direct Payment mechanism. At a farm level, this means that 27% of farm-income comprises Direct payment subsidies[2]. Even more stark is the variation of this figure across crops. For Cereal and other field crops, the share of subsidies has varied from 40% to 80% between 2007 and 2015, underscoring their role as a cushion against farm income volatility[3].

Fig 1. Direct Payments per hectare in Europe - 2015

Fig 2. Direct Payments as a % of Farm income by country

A complicated lifeline

The process for paying out Direct Payments subsidies reflects the tension between centralized policy making and localized implementation that is a consequence of the principle of subsidiarity espoused by the EU. Country-wise allocations for the subsidy budget are made in Brussels but the implementation of payments is the responsibility of individual countries. In addition, there is a multiplicity of schemes to achieve the various goals that European agriculture aspires for. The eligibility criteria and data submission requirements for these schemes are under the jurisdiction of individual countries who need to put in place procedures and systems to receive and process aid applications. Thus, at an implementation level, the CAP is characterized by widely divergent procedures and data requirements that make it very difficult to create a single continent-wide scalable solution.

The need for digitization

Given the significant reporting requirements of the subsidy process, it is surprising that farm digitization and adoption of Farm Management Software packages has not been as rapid as one would suppose. At €266/ha, the value pool addressable through a more seamless farm management and documentation system is substantially higher than the returns of yield improvements typically promised by digital tools in the market. Neither is there an unwillingness of growers to avail external services to support this process – growers across Europe pay for consultant support for this process. The only way to explain this visible market failure is to conclude that many FMS and digital packages today do not provide growers with tools that help them with their real requirements. While FMS packages in Europe provide growers with combinations of precision ag data sets (satellite imagery, drone imagery), accounting modules and product registration information, there doesn’t seem to be yet a software package that closes the loop between data input and report generation. Additionally, most FMS players are single country focused and the challenges of multiple languages, regulations, and channel structure make scale-up difficult.

An opportunity beckons

Given the above situation, there is clearly a need for digital solutions in Europe, just not the ones that are on offer. In addition, the new CAP 2020 policy is likely to provide an impetus on responsible farming practices by linking pay-outs to demonstrated and documented farming practices. Companies that look to develop a solution that is customized to the economics of farming in Europe will succeed – those who try and push ‘technology for the sake of technology’ will have a tough time.

Notes:

[1] ’CAP Explained – Direct Payments for Farmers 2015-2020’, published by EU

[2] ‘Share of direct support in agricultural factor income - 2016’ sourced from https://agridata.ec.europa.eu/extensions/DashboardIndicators/FarmIncome.html

[3] ‘Operating Subsidies’ published by DG Agriculture and Rural Development, EU